You’re scrolling through your banking app, feeling pretty good about that 760 credit score staring back at you. You walk into the bank, confident you’ll get the best mortgage rate. Then boom—they tell you your “actual” score for the mortgage is 700.

Wait, what?

If this sounds familiar, you’re not alone. And honestly? You’ve just stumbled into one of the mortgage industry’s best-kept secrets.

Here’s the kicker: 73% of people can boost their credit score by 20+ points in just 30 days using techniques that mortgage brokers use every single day. We’re talking about potential savings of $39,292 across all your debt, with over $31K of that coming from your mortgage alone.

So why don’t banks tell you this stuff? Simple. They don’t have to.

The Credit Score Shell Game Nobody Talks About

🎭 The Credit Score Reality Gap

Let’s start with the most mind-blowing fact: The credit score on your phone is probably 20-60 points higher than what mortgage lenders see.

I know, I know. It sounds crazy. But here’s what’s happening behind the scenes.

While you’re checking your shiny FICO Score 8 on your banking app (the modern version), mortgage lenders are stuck using ancient algorithms from 2004. Think of it like this: you’re driving a 2024 Tesla, but the lender is evaluating you based on a 2004 Honda Civic.

Why This Happens (And Why It Matters)

Fannie Mae and Freddie Mac—the government-sponsored entities that buy most mortgages—haven’t updated their requirements in decades. They still require lenders to use FICO Scores 2, 4, and 5.

These old scores are harsher. They don’t consider:

- Medical debt improvements

- Rental payment history

- Recent algorithm updates that benefit consumers

Real example: Sarah from Atlanta saw 760 on her app but qualified at 700 for her mortgage. That 60-point difference could have cost her thousands in higher interest rates.

The Tri-Merge Trap

Here’s another curveball: lenders don’t just look at one score. They pull from all three credit bureaus (Experian, Equifax, TransUnion) and use your middle score. If you’re buying with a partner, they use the lower of your two middle scores.

So even if two of your scores are great, one lagging score can tank your rate.

Why Mortgage Brokers Are Playing a Different Game

Ever wonder why some people seem to get amazing mortgage deals while others struggle? Often, it comes down to who they’re working with.

Recent data shows brokers save customers an average of $10,662 over the life of their loans compared to going directly to banks. But the real magic isn’t just in shopping rates—it’s in their credit optimization toolkit.

Brokers Have Secret Weapons

While banks say “come back in six months” to improve your credit, brokers have access to platforms that can run hundreds of credit scenarios instantly. These tools show exactly what actions will boost your score the most.

Mike Darne from CreditXpert puts it perfectly: More than 50% of people rejected for low credit scores could qualify within just 30 days using optimization techniques.

But here’s the thing—most banks don’t offer these tools to their customers.

The Rapid Rescoring Advantage

This one’s huge. Rapid rescoring can increase your score by 100+ points in 3-5 business days. It costs around $75-120 total but can save you $3,000-5,000 in loan costs.

That’s a 2,500% return on investment.

Most banks? They don’t even offer this service. They’ll tell you to wait months for improvements to show up naturally.

Real People, Real Results

Let me share some stories that’ll blow your mind.

Case Study #1: A client in Oregon had a 678 mortgage FICO score. Their broker identified one problem: a credit card with a $3,595 balance. They paid it down to $231, and their score jumped to 720—a 42-point increase. This simple move saved them $5,000 in loan costs.

Case Study #2: Another borrower saw an 81-point increase in 33 days just by strategically paying down high-utilization credit cards. The result? $3,000 savings on a $200,000 loan.

These aren’t unicorn stories. This happens every day in the mortgage world.

The Broker vs. Bank Numbers Don’t Lie

Let’s talk cold, hard data for a second.

Polygon Research analyzed 2023 mortgage data and found:

- Average broker rate: 6.26%

- Average bank rate: 6.40%

That 0.14% difference might seem tiny, but on a $400,000 mortgage, it’s about $34,000 over 30 years.

Approval rates tell an even more interesting story:

- Brokers: 75% approval rate

- Banks: 64% approval rate

In minority communities, the gap widens further. Brokers help borrowers who might otherwise get rejected by traditional bank underwriting.

Your Step-by-Step Credit Optimization Game Plan

🎯 4-Month Credit Optimization Roadmap

Ready to take control? Here’s your action plan.

Step 1: Get Your Real Scores

Forget the free apps. You need to see what mortgage lenders see.

Go to myFICO.com and pay $19.95 for one month. Get your FICO Scores 2, 4, and 5. These are your mortgage scores. This small investment could save you thousands.

Step 2: Master the Utilization Game

Credit utilization is huge for your score. But here’s what most people don’t know: you want to be under 10%, not just under 30%.

Quick wins:

- Pay down your highest-utilization cards first (ignore interest rates for now)

- Request credit limit increases on all cards before applying

- Spread balances across multiple cards instead of maxing one out

Step 3: Time Everything Right

The golden rule: Complete all your credit optimization 30 days before applying for a mortgage. This gives the new information time to hit your reports.

When you’re ready to shop for rates, do it within a 14-day window. Multiple mortgage inquiries in this timeframe count as just one inquiry on older FICO models.

Step 4: Find a Broker Who Gets It

Ask potential lenders these specific questions:

- “Do you offer rapid rescoring services?”

- “Can you run credit simulations to show me improvement options?”

- “What’s my qualifying score versus my individual bureau scores?”

If they can’t answer these confidently, keep looking.

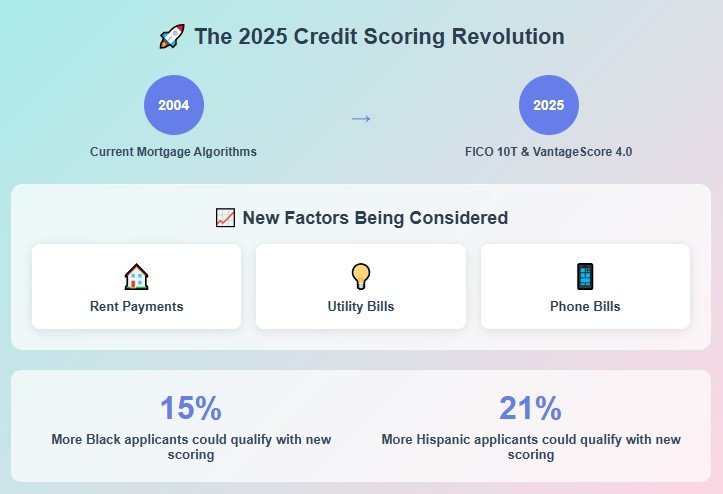

What’s Changing in 2025 (And Why You Should Care)

Here’s something most people don’t know: The biggest change to mortgage credit scoring in decades is happening in late 2025.

Lenders will start using FICO 10T and VantageScore 4.0. These new models will consider:

- Rent payments

- Utility payments

- Telecom payments

This could help 15% of previously denied Black applicants and 21% of denied Hispanic applicants qualify.

If you pay rent, utilities, or phone bills on time, start documenting these payments now. You’ll want this history when the new models go live.

The Bottom Line: Knowledge is Power (And Money)

Look, the mortgage industry isn’t exactly known for transparency. But now you know what brokers know.

The tools exist. The strategies work. The data proves it.

Every month you wait with a suboptimal credit score costs you money. Not just on your mortgage, but on car loans, credit cards, and even insurance rates.

Your Next Move

Don’t let another month go by wondering “what if.”

Here’s what to do right now:

- Get your real mortgage scores from myFICO.com

- Find a broker who offers credit optimization tools

- Run the numbers to see your potential savings

- Start optimizing your credit strategically

Remember: 73% of people can improve their scores significantly in 30 days. The question isn’t whether you can do it—it’s whether you will.

Your future self (and your bank account) will thank you.

Ready to unlock your credit’s true potential? The strategies in this article have helped thousands of borrowers save tens of thousands of dollars. The only question is: Will you be next?